Market Summary

Construction Plastics Market Overview

The Construction Plastics Market Size was valued at USD 112.25 Million in 2023. The construction plastics industry is projected to grow from USD 121.94 Million in 2024 to USD 233.59 Million by 2032, exhibiting a compound annual growth rate (CAGR) of 7.95% during the forecast period (2024 - 2032). Construction plastics are plastics that are chemically treated to make them suitable for construction purposes. Construction plastics come in different forms such as wood-plastic composites, Luxury vinyl tiles, and significant others. Some of the benefits of using construction plastics are lower maintenance, scratch resistance, lightweight, higher strength, and flexibility are considered as the major factors that are driving the overall growth of the construction plastics industry in recent years. Also, experts have observed significant competition in the building and construction industry across the globe that is also stimulating the construction plastics market growth.

The abundant availability and the affordability of plastics and other favorable environmental factors are presenting lucrative opportunities for construction plastics market growth. Among other types of construction plastics, polyvinyl chlorides are intensively utilized for pipes across the construction sector. The potential characteristics such as thermal conductivity, insulation, durability, long life, the capability of adopting varied designs, ergonomic, scratch resistance, and much more of polyvinyl chloride are propelling the construction plastics market in recent years.

Construction Plastics Market COVID-19 Analysis

The demand for construction plastics is higher in the countries such as China, Indonesia, and Brazil. However, during the pandemic, these were the countries that were severely affected. Such factors have significantly affected the overall growth of the construction plastic industry. Also, the construction activities across the globe were severely affected due to the movement restrictions imposed by the government of several countries. Such factors have also negatively influenced the construction plastics industry during the pandemic.

The decline in the oil and gas industries in the developed regions has also impacted the manufacturing of construction plastics. However, on the other side, the demand for the construction applications such as smoke detectors and fire detectors have intensively utilized construction plastics, for crucial infrastructural development such as hospitals and medical centers. Such factors have supported the overall growth of the construction plastics industry during the pandemic.

Market dynamics

Market drivers

The major drivers for the construction plastics industry are their potential characteristics. There are several beneficial characteristics such as effective insulation for the cold and hot weather and thereby conserve energy effectively. Such factors are major drivers of construction plastics market growth.

The increasing urbanization, advancement in technologies, and emphasis on recycling procedures are considered as the major market drivers of the construction plastics industry.

Market opportunities

The increasing construction activities across the developed countries such as North America and Europe due to the higher disposable income and inclination towards sophisticated infrastructure and interiors are expected to boost the overall growth of the construction plastics industry during the forecast period.

The demands for construction materials that can lift heavy materials and the cost-effective processes in the construction sector are higher. Such factors are propelling the demand for polystyrene which is considered as the poor conductor of heat and retains energy longer. Such factors are expected to impact the construction plastics market growth during the forecast period.

Market restraints

The raw materials required for the manufacturing of ethylene, propylene, and styrene are highly dependent on crude oil, which tend to fluctuate severely. Therefore the increasing costs of crude oil significantly affect the construction plastics market growth.

The stringent regulations related to plastic production, imposed by the governments of certain developed countries are expected to hinder the construction plastics market growth during the forecast period. Similarly, the increasing demand for green buildings in developed countries is decreasing the demand for PVC products and is considered as the potential restraint of construction plastics market growth.

Market challenges

There are very few efficient standards for the construction plastics industry and the workforce in the construction plastics industry are considered poorly skilled. Such factors are considered as the major challenge for the overall growth of the construction plastics industry.

The return of investment for the manufacturers of these construction plastics is also considered the major challenge. For instance, the price of the construction plastic materials are comparatively lesser than other materials, however, the manufacturing processes require several stages such as CNC machining, polymer casting, rotational molding, and significant others.

Cumulative growth analysis

The construction plastics market value was at USD 105.67 billion in 2022 and it is expected to surpass the market value of over USD 200.45 billion by the year 2030 while registering a CAGR of 7.59% during the forecast period. This market estimate is due to the lower costs of the construction of plastic materials over other alternatives. Thermosetting plastics are used intensively in construction activities because of their characteristics such as blending, toughness, flame resistance, strength, easier processing, flexibility, and significant others. Therefore they are used for the window and skylight, cladding panels, canopies, roof domes, and other construction requirements.

The role of construction plastic market has been expanded to wide areas in the construction sector in recent years and has seen an evolution in the technological world. Moreover, the unavailability of competitive materials in the place of these construction plastics is boosting the overall growth of the construction plastics industry.

Value chain analysis

Among other construction plastics materials, polyvinyl chloride is prominently used in the construction plastics industry, whereas the others are considered to be less cost-effective. The pipings, window applications, and other areas are major consumers of polyvinyl chloride material due to its potential characteristics such as thermal conductivity, scratch resistance, and as it allows varied options to design them. The increasing trend and technologies in the construction industry and the amount of sophistication the customers look for are propelling the construction industries to look for better and cost-effective materials for construction purposes. There are multiple ways to utilize construction plastics in huge volume that helps in generating revenues for the construction plastics industry.

Also, several developed countries are focused on construction activities, both residential and commercial infrastructure, which provides lucrative opportunities for the overall growth of the construction plastics industry. Also, the developed countries are emphasizing the recycling of plastics in every possible way, which has again offered opportunities for the research team to further propel the construction plastics market growth across those countries.

Segment overview

Based on plastics

- Expanded polystyrene

- Polyethylene

- Polypropylene

- Polyvinyl chloride

- Others

- Acrylic sheets

- Polycarbonate sheets

- Reinforced plastics

Based on the plastic-type

- Polystyrene

- Polyethylene

- Polypropylene

- Polyvinyl chloride

- Others.

Based on the application type

- Pipes

- Windows & doors

- Insulation materials

- Others.

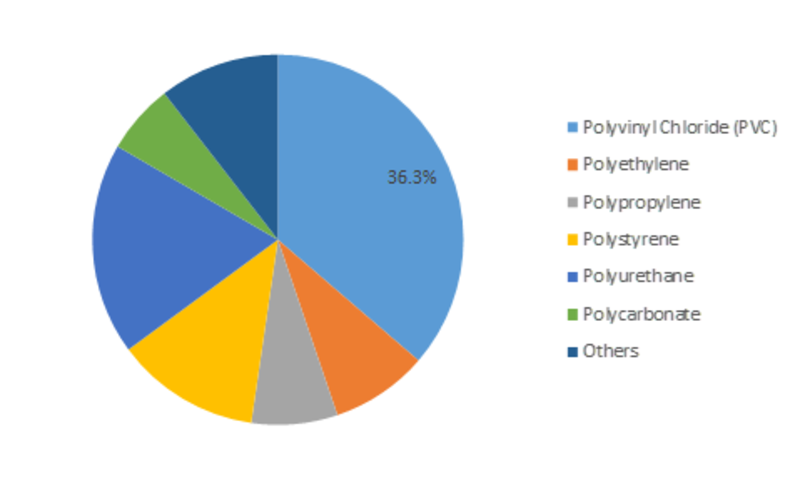

Global Construction Plastics Market Share, by Type, 2017 (%)

Source: MRFR Analysis

Regional analysis

Currently, Asia-pacific is holding the highest construction plastics market share among the other potential regions. The market growth is due to the increasing adoption of construction plastics in the countries like China and India. China is considered the largest producer of polyurethanes plastic materials and thermoplastics, and the country also exhibits increasing industrialization and urbanization. The production capacity in China rises year over year at affordable rates and labor is also driving the overall growth of the construction plastics industry across the region.

Similarly, the favorable conditions for construction plastics market growth such as supporting government policies, cheap labor, abundant natural resources, industrial facilities, and significant others are creating an impact on construction plastics market growth.

Competitive landscape

- DowDuPont (US)

- BASF SE (Germany)

- Asahi Kasei Corporation (Japan)

- LyondellBasell Industries Holdings B.V. (Netherlands)

- Borealis AG (Austria)

- Solvay S.A. (Belgium)

- Berry Plastics Corporation (US)

- Total S.A. (France)

Recent developments

BASF SE made an announcement on February 2023 that it will enhance its production capacity for Neopor® Expandable Polystyrene (EPS) insulation to meet the rising demand of energy conserving building materials.

Solvay S.A. presented Technyl® 4earth®, a range of eco-friendly polyamide (P.A.) materials aimed at sustainability in construction through recycling of plastic waste on November 2022.

Borealis AG unveiled Borstar® R3BX pipe solution in September 2022 that strengthens plastic piping systems used in construction and infrastructure projects by increasing their performance properties and service life.

In May 2022, Dow introduced its AGILITY™ performance LDPE resin which is aimed at enhancing toughness and impact resistance in building applications.

Asahi Kasei Corporation launched Thermylene® P11 thermoplastic resin for automotive and building applications with improved rigidity and heat resistance in January 2022.

LyondellBasell Industries Holding B.V. bought A. Schulman, Inc., one of the world’s most reputable suppliers of engineered plastics, composites as well as powders in August 2021.

Berry Plastics Corp announced completion of acquisition Clopay Plastic Products Company Incorporation producer of breathable films and laminates for various industries July 2021.

In March 2021, DuPont launched Tyvek® Air and Water Barrier products that can improve building envelope protection by improving both energy efficiency as well as moisture management

Report Overview

This report has covered

- Market overview

- COVID 19 Analysis

- Market dynamics

- Cumulative growth analysis

- Value chain analysis

- Segment overview

- Regional analysis

- Competitive landscape

- Recent developments

Segmentation Table

Based on plastics

- Expanded polystyrene

- Polyethylene

- Polypropylene

- Polyvinyl chloride

- Others

- Acrylic sheets

- Polycarbonate sheets

- Reinforced plastics

Based on the plastic-type

- Polystyrene

- Polyethylene

- Polypropylene

- Polyvinyl chloride

- Others.

Based on the application type

- Pipes

- Windows & doors

- Insulation materials

- Others.

Market Size & Forecast

| Report Attribute/Metric | Details |

| Market Size 2023 | USD 112.25 Million |

| Market Size 2024 | USD 121.94 Million |

| Market Size 2032 | USD 233.59 Million |

| Compound Annual Growth Rate (CAGR) | 7.95% (2024-2032) |

| Base Year | 2023 |

| Market Forecast Period | 2024-2032 |

| Historical Data | 2018 & 2020 |

| Market Forecast Units | Value (USD Million) |

| Report Coverage | Revenue Forecast, Market Competitive Landscape, Growth Factors, and Trends |

| Segments Covered | Type, Application |

| Geographies Covered | North America, Europe, Asia Pacific, and the Rest of the World |

| Countries Covered | The U.S, Canada, Germany, France, the UK, Italy, Spain, China, Japan, India, Australia, South Korea, and Brazil |

| Key Companies Profiled | BASF SE (Germany), DowDuPont (US), PetroChina Ltd (China), Borealis AG (Austria), Solvay SA (Belgium), Arkema (France), SABIC (Saudi Arabia), B & F Plastics, Inc., (US), Cork Plastics (US), and Trinseo (US) |

| Key Market Opportunities | Rapid urbanization and industrialization |

| Key Market Dynamics | Increasing construction activities and HVAC market |

Leave a Comment